The dealership business is the only segment that is low to moderately cyclical across the entire automotive supply chain. Large franchise dealers like Group One Automotive (GPI) and Lithia Motors (LAD) benefit from cost economies, centralized back-office and intangible advantages like customer retention, regulation and technology. In addition, Lithia and Group One are actively acquiring smaller independent dealers, aiding them to benefit from the consolidation. Although dealership is a low margin business, on average, 50%-65% of LAD and GPI margin is derived from economically less sensitive segments such as part & service and used vehicles. Apart from the obvious hit due to COVID-19, these two dealership stocks provide great risk-adjusted returns for patient investors, at current levels.

Note: At the time of this article LAD was trading at around $83 (52-week low) and GPI at around $50 (4-year low).

Used Vehicle and Repair & Service Segment

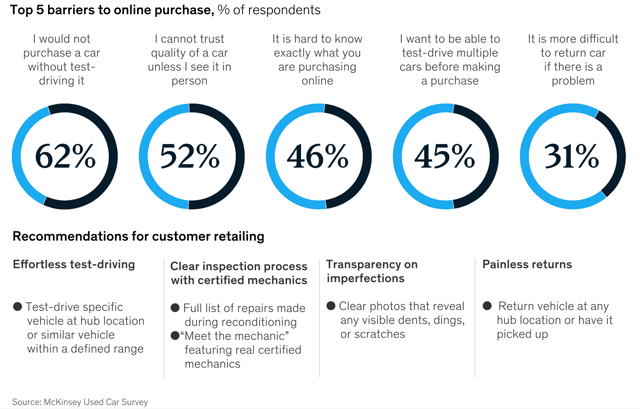

There's no doubt that online entrants like Carvana, Shift, Vroom etc., are eating into auto dealers revenue and margins, but traditional players like LAD and GPI have non-digital advantages over online players like the ability to conduct test drivers, in-person inspections and repairs/service. McKinsey research shows that more than 60+% of customers prefer to do business in-person.

(McKinsey)

Repair & service business protects dealers from economic headwinds as spending is need-based rather than discretionary, which creates inelasticity of demand, that in turn creates a stable source of revenue for dealers in good times and bad. There's no doubt that the pandemic has created a lot of chaos, with 40%- 50% of customer pausing new/used vehicle purchases for 3-6 months and more than 70% consumers delaying service and maintenance due to social distancing efforts, based on the research conducted by COX Automotive. As things get back to normal (hopefully soon), I think consumers would hesitate to buy a vehicle for while due to lost jobs/income and decline in confidence. This will definitely hurt auto manufacturers, but I think incumbent large dealers like Lithia and Group one won't be affected as much.

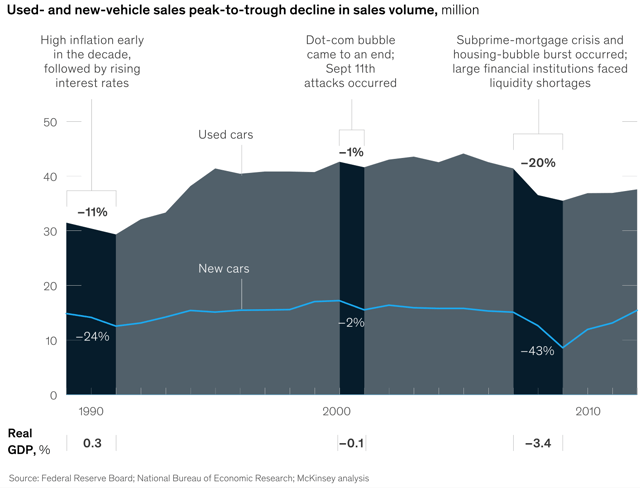

New car sales will certainly take a hit in 2020, but used car sales are less vulnerable to recessions and shocks. As McKinsey points out that- "Used cars offer a relatively countercyclical safe harbor from the dramatic sales highs and lows seen among new vehicles, with peak-to-trough declines averaging about 11 percent over the past two decades, compared with 23 percent for new ones". Below chart from explains this:

(McKinsey)

(McKinsey)

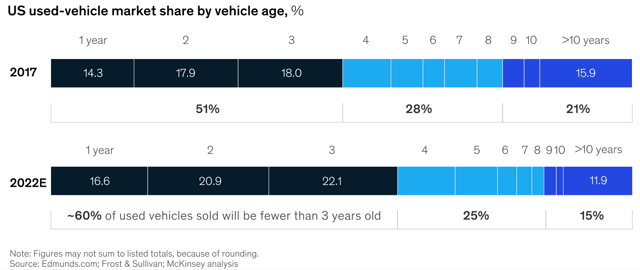

Unsurprisingly, the used car market is twice the size of the new car market, and franchise dealers still own a majority of the used-car market. McKinsey research also shows that "used vehicles are becoming increasingly younger in a shift largely driven by greater off-lease supply and newer certified pre-owned vehicles".

(McKinsey)

(McKinsey)

With diminishing outlook in 2020 and 2021, I think financially strong consumers would most likely buy an off-lease certified pre-owned (CPO) vehicle from dealers instead of a brand new one. Cox Automotive expects that small to mid-sized car owners would most likely purchase off-lease SUV, pickups and CUVs, due to increasing demand for these vehicle type. This would result in a positive outcome for LAD and GPI, as pre-owned vehicles are sold at higher margins than brand new ones, and large dealers dominate the sales of CPOs or vehicles that are 0-4 years old. Over the past few years, more and more consumers are buying SUVs, Crossovers (CUV) and light trucks. The SUV segment is expected to grow to nearly 50% of the automotive market, by the end of 2022. This rise in demand for used SUV, trucks and CUV purchases would cause the average price of a pre-owned vehicle to rise, contributing to Lithia's and Group One's used vehicle margins. Although new vehicle sales take a hit, these factors should stabilize LAD and GPI used vehicle sales going forward. Lastly, expansionary monetary and fiscal policies in response to COVID-19 shall provide a boost to LAD and GPI's financing business (F&I), which is a 100% gross margin segment.

Lithia MotorsLithia Motors and Group one stocks are heavily beaten down, as sales are expected to decline this Q1 and Q2 due to COVID-19 and lockdowns across the country. While the end of lockdown period and COVID-19 pandemic are still uncertain, LAD and GPI generate most of the margins from repair & service, used vehicle and F&I segments, which provide some cushion in a zero to negative growth environment. Around this time last year, I wrote an article on Lithia Motors here, by the end of 2019 the stock more than doubled trading at around $130-$135, from $65-$70 per share (at the beginning of 2019). At the time of this article, the stock was trading at close to its 52-week lows. I expect a similar rebound by the end of 2020, assuming a positive 2021 management guidance.

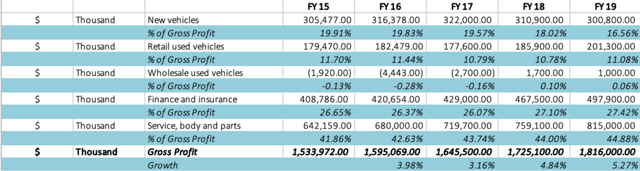

(From 10-K)

(From 10-K)

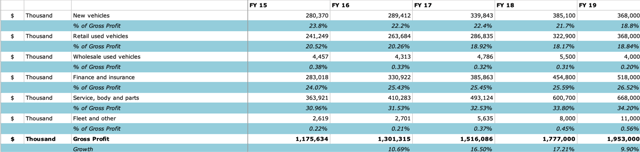

As you can see from the above, almost 50% of the gross margins are derived from service and used car segment. Used car YoY gross margin as a percentage of total gross profit confirms that online players have an impact on LAD's used car margins. However, the decline was offset by growth in the service segment (CAGR 2.02% vs -1.69% used vehicle CAGR). With interest rates at 10-lows and used vehicle sales expected to gain traction, it should counterbalance further declines new car sales and the F&I sales.

Rural Market Focus

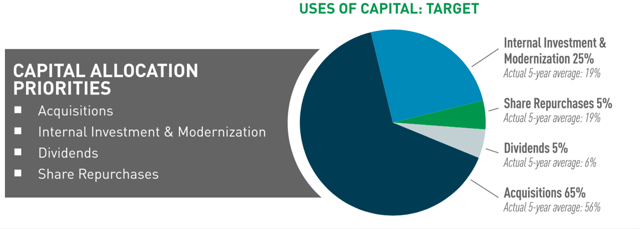

Lithia primarily serves in rural markets where those markets are predominantly ignored by large players, as they target suburban areas. For example, in Anchorage (Alaska's largest city), there are four Chevrolet stores and the company owns three of them. Across the US, majority of Lithia stores don't have any close competitors within a 100-mile radius (partly due to franchise laws/rights and regulations). Also, the company is actively acquiring smaller dealers across these underserved rural areas, with acquisitions being the top capital allocation priority after maintenance capex. These factors should give Lithia some pricing power, countering any declines in new vehicle sales.

(Source: Q4 Investor Presentation)

In addition to that, non-urban areas are less affected by broader emerging trends within the dealership space (ex, online selling/e-commerce), as individuals tend to stick with traditional dealerships due to the slower adoption to innovation. However, to compete with online players, LAD invested $54MM in online used car sales company Shift to become the largest shareholder. This gives the company access to technology and valuable data that it likely could not be developed on its own.

Location

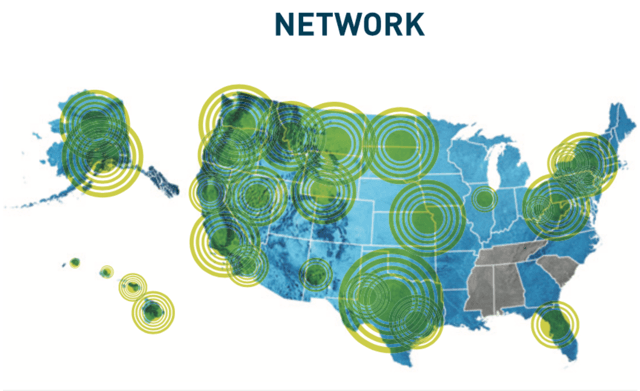

Lithia hasn't provided a lot of info regarding its store locations but the picture below indicates that the firm has approximately half of its stores located in colder parts of the country. Generally, vehicles in colder regions require service/repair more often than vehicles located in warmer regions.

(Source: Q4 Investor Presentation)

Lithia's double-digit revenue and stable gross margin growth numbers are not only reflective of the company's strong business model but also its customer service capabilities. According to Businesswire, "Lithia had 45 stores win the 2020 DealerRater Consumer Satisfaction Award". These awards are based on reviews on pricing, service, quality of work and overall experience.

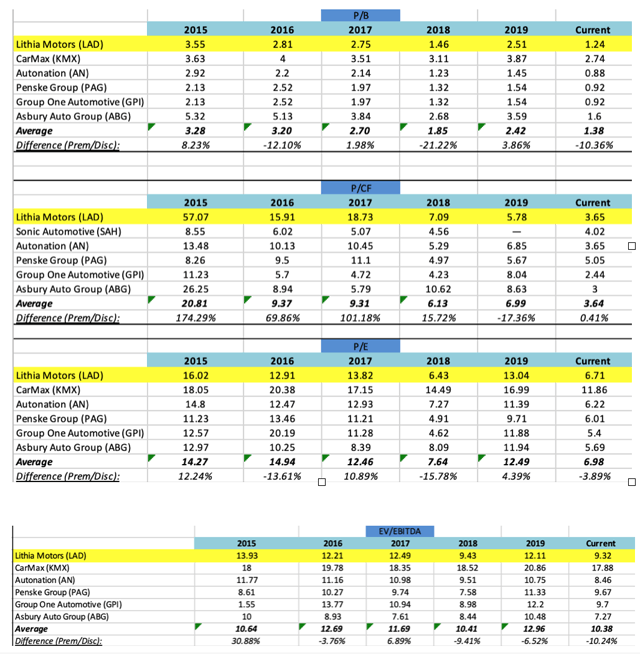

(Data from Morningstar)

(Data from Morningstar)

The price and EV/EBITDA multiples don't provide great insight into LAD's multiples relative to the peer average, as historically they were choppy. Although competitors won't represent the entire industry, I think it's a good proxy for LAD since they have very similar business models and target market. The current P/B, P/E and EV/EBITDA multiples suggests the company is trading below competitor averages. Aside from P/CF, every time LAD traded at a discount to its peers, the multiples expanded and the stock traded close to its peers or slightly at a premium.

Financial Strength (As the end of 2019)

(From Morningstar and 10-K)

Although financial leverage is slightly high, the company is will realize extra revenue gained from its acquisitions and it should offset in a rise in interest expense.

Operational Efficiency

(Source: 10-k and Morningstar)

Generally, dealerships tend to have fairly high operating leverage due to fixed costs. Lithia has managed to reduce operating leverage from 1.48 to 0.67 over the past five years, allowing for a variable or flexible cost structure. Low Op. leverage won't maximize returns but it provides enough cushion for the management to cut costs during uncertain times like we are facing right now.

SG&A as a percentage of gross profit is a common operating metric in the dealership space. LAD's ratio has been close to 70% over the past five years, it shows that the management is managing operating costs efficiently. If the ratio falls below 70% of gross profit, there's potential for EBIT margin improvement.

Group One Automotive (Source 10-K)

(Source 10-K) Similar to Lithia Motors, GPI generates 50+% of its margins from used vehicles and service segment. In 2018, Group One implemented a new strategy called Value-U-Line strategy that primarily sells high mileage used vehicles for retail customers, instead of selling them through an auction or wholesale. The former is a lot more profitable and it could reach 15%-20% of gross profit from 11% in the next couple of years.

Digital Initiatives

Besides implementing Value-U-Line strategy, the company also created an online platform called AcceleRide for used and new vehicles. The recent investor presentation claims that "during 4Q19, AcceleRide grew by a rate of 3x its usage from 1Q19. AcceleRide's closing rate is pacing more than double that of a third party lead", and "nearly 29% of our service appointments were made online". The digital initiate should help improve used and repair segments.

Aftersales Market Sales

Same-store parts & service revenue rose 7% in 2019, as the company implemented "four-day workweek service schedule that has increased capacity in a significant number of our service departments" and it allowed them "to improve recruiting and retention efforts with service technicians and service advisor professionals". (Q4 Investor Presentation). These initiatives should provide another boost to the P&S and used car market segment.

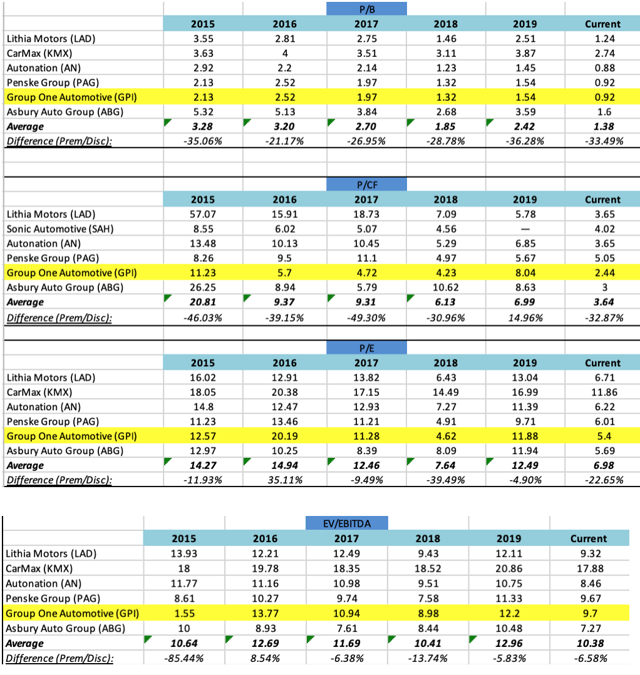

(From Morningstar)

(From Morningstar)

Price and EV/EBITDA multiples suggest that GPI historically traded below the peer average. I believe the market underpaid GPI relative to its peers because the firm doesn't have a strong differentiating factor, like Lithia Motors. But I think GPI is better positioned to ride through an economic downturn, considering that it has a strong balance sheet and management's new initiatives to strengthen the high margin-low cyclical segments (parts&service/Used-vehicle).

(From Morningstar)

GPI's leverage ratios look manageable but the interest coverage ratio is below Lithia's, which provides a lower cushion in a downturn.

Operational Efficiency:

(From Morningstar)

(From Morningstar)

GPI's operating leverage is all over the place and management hasn't done a great job in keeping costs lower (SG&A as a percentage of gross profit), compared to Lithia. However, the company's "total parts & service gross profit covers 90-95% of total company fixed costs and parts & service selling expenses" (Q4 Investor Presentation). I think this should provide enough flexibility for the management to cut variable expenses in case of a sudden decline in new/used vehicle and F&I sales.

ConclusionApart from the obvious risks due to lockdowns and social distancing, both the companies are financially strong with some flexibility around operating leverage. Lithia and Group one generate 50+% of gross margins from economically low cyclical segments and both management teams implemented initiatives to grow repair & service and used car segments. With favorable trends in the used car sales market (off-lease/CPO) and GPI/LAD's strong foothold in after-sales repair & service market should provide enough downside protection in a declining outlook across the automotive industry.

Disclosure: I am/we are long GPI. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article. Additional disclosure: Initiated position in Lithia Motors at $80 per share (5th April) and Group One Automotive at $53 per share (on 7th April).

Komentar

Posting Komentar